Blockchain To The Rescue -- How We Can Fix Our Fragmented Banking System

We found blockchain's killer app -- it's interoperability -- and it will break down data silos and bring our fractured financial system together

Banks keep their data in silos, which leads to mistakes and poor performance, and customers wind up paying the price

Blockchain can fix this by improving “interoperability,” aka improving data sharing by replacing data silos with a single shared ledger

Over the next three years, Banks worldwide are moving to a new data standard, ISO 20022, that will incorporate blockchain to improve interoperability

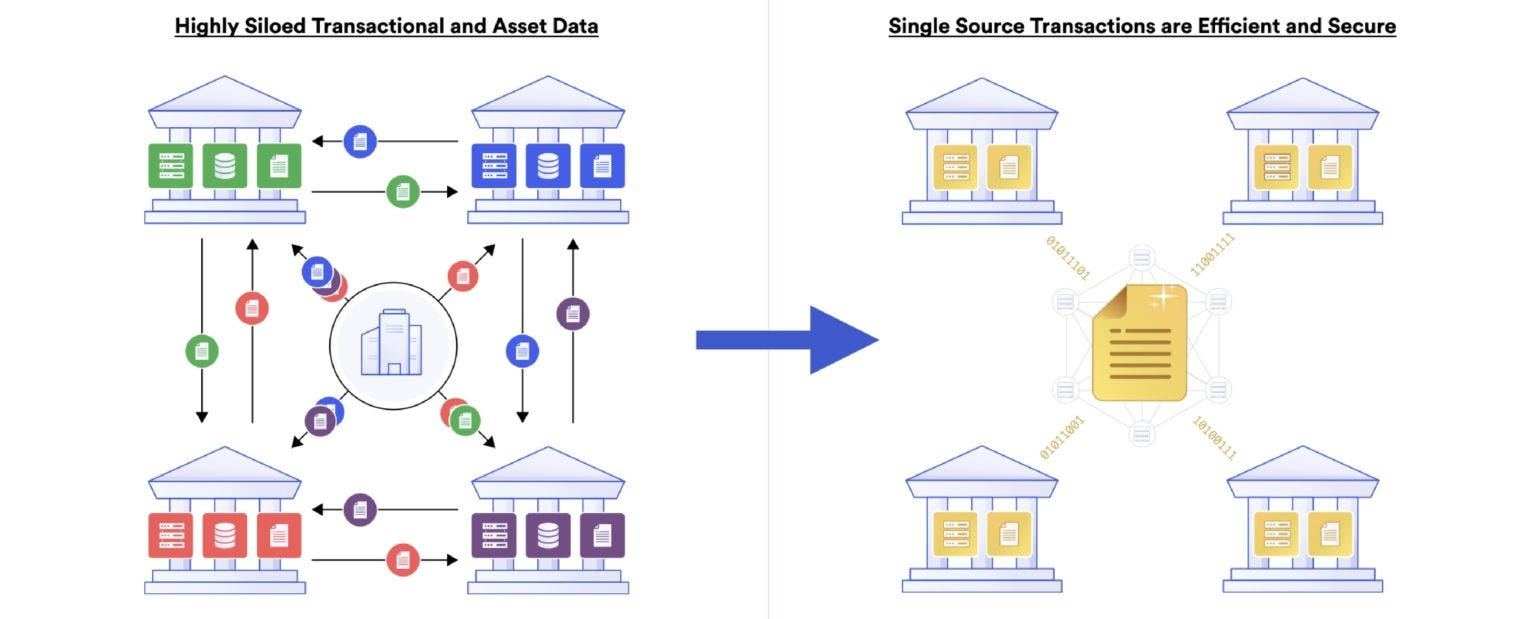

Fragmentation of the Banking System is the Problem, and Interoperability — Built on Blockchain — Is the Solution

Have you ever had a bank screw something up royally, and then you had to spend weeks or months trying to get it straightened out?

The problem is banks don’t play well with others. They send money to the wrong people, hold on to your money, don’t catch fraud, and then blame you.

But Blockchain can and will fix this.

Many of the problems with our financial system come down to a bunch of institutions that don’t trust each other and don’t work well together. In other words, what we need, but don’t have, is financial “interoperability.”

But blockchain fixes that. In fact, interoperability is blockchain’s killer app.

What is the “Financial Interoperability” Problem?

Financial interoperability means the ability of different financial systems and institutions, such as banks, to work together seamlessly. In other words, financial interoperability is what allows different financial systems to “speak the same language,” break down silos and communicate with each other effectively.

Anybody who has spent time with banks will tell you that they don’t always communicate with each other effectively. They don’t “play well with others.”

Do any of the following sound familiar?

Sheila the Student qualifies for a government grant that will pay her tuition and fees so long as she goes to an accredited school. Her school is accredited, but for some reason, her bank doesn’t believe that, so it won’t release the money. Meanwhile, the school is demanding payment, and Sheila is caught in the middle.

Barbara the Business Owner accepts payment by check, but the check bounces. When Barbara accepted the check, she called the bank to confirm, yet somehow the check still bounced. Now Barbara gets caught in the middle between her bank and the customer’s bank.

Ron Rice the Renter had his rent check bounce. Turns out that when Ron’s bank received his paycheck deposit, they credited it not to him, “Ron Rice,” but to Rowan Reis, i.e., another customer with a similar name. So, due to the bank’s mistake, Ron’s payment check bounced for insufficient funds. Oops, sorry, Ron. Two months later, after much wasted time and the bank – as a “courtesy” – waiving fees, it was resolved. Some courtesy.

Mike wrote a check to pay his student loans, but the financial institution servicing the loan changed, and he spelled the name wrong and got the zip code wrong. The bank calls this “user error.” But any time a “user error” happens repeatedly, that’s a design error, not a user error. User-centered design should account for, help catch and prevent, and correct normal errors.

Cate was canceling her account with her bank and gave the bank two months’ notice. She was very careful to contact as many of her accounts as she could to make sure they knew her new account information. The bank promised her that it would close her account and promised her that — even if a few payments slipped through the cracks — the bank would not make any more payments from her account. Despite the bank’s promises, a few more electronic payments came through, and the bank paid them, so Cate’s account had a negative balance.

Frank the Fraud Victim’s debit card was stolen and used without his consent. The bank did not catch the fraud until Frank reported it. Frank informed the bank that he was on the other side of the country from the gas station where the account was used, but the bank needed to investigate. It took three months to get the money back into Frank’s account.

All of these stories have an underlying pattern. In each case, the bank miscommunicated or had wrong information, or didn’t trust correct information, and so a payment was delayed, misrouted, or otherwise mishandled. In each case, the bank’s information was in a silo, and the information the bank needed to correct or avoid the problem was in another silo.

Our entire banking system depends on banks sending messages back and forth with other banks and other institutions, but the banks can’t trust each other. So they need to check and doublecheck these communications, often manually. And this leads to mistakes and delays.

Blockchain, or distributed ledger technology, fixes this because it replaces (1) data silos held by institutions that don’t trust each other, with (2) a single ledger, shared by all the relevant institutions.

connecting old systems to each other -- like translating pounds from the Bank of England into Yen from the Bank of Japan

connecting old systems to new systems -- like translating US Dollars to Central Bank Digital Currencies

connecting new systems to each other -- like translating CBDCs to tokenized bonds

Better Interoperability Will Break Down Silos and Make the Whole System More Efficient

For Sheila the Student, interoperability eliminates the dispute about whether her school is accredited. The government and the school can verify that she is still enrolled and that the payment has been made.

For Barbara the Business Owner, better interoperability means she no longer has to deal with paper checks and no longer has to worry about bounced checks. The customer’s bank and her bank can share information immediately about the customer’s balance and transfer the money much faster.

For Ron the Renter, better interoperability means much better data, which should eliminate or at least vastly reduce the chance that a payment meant for him winds up in the account of someone else with a similar name. More data means more redundancy, and much better error correction and prevention.

For Mike, who made a mistake when he specified the wrong institution name and wrong address, better interoperability means better data which means that the bank can do more to help him. In fact, perhaps Mike wouldn’t even need to specify the recipient – when his account was sold to a new servicing company, all of the information could be updated behind the scenes and checked and double-checked.

Similarly, for Cate, who canceled her account, better interoperability means that she can smoothly and easily transfer her account and her account information to all her creditors. And would make it much easier to connect her new account to her old account so that any requests for payment that came through could be seamlessly transferred to her new account. Meanwhile, all the creditors could be updated seamlessly with newly updated account and contact information for her.

For Frank, whose debit card was hacked, better interoperability means that multiple banks and institutions can share data, and share data and use sophisticated algorithms to detect and prevent fraud. It also means that information between institutions travels instantly, rather than through intermediaries, making it easier to spot fraudulent transactions immediately.

Better interoperability also makes it easier for the average person to transfer funds with fewer mistakes and at less expense. It also makes it easier, for example, to transfer funds directly rather than going through a bank

ISO 20020, the New Data Standard, Is Coming

Right now, banks around the world are transitioning to a new global standard for financial messages called ISO 20022.

ISO 20022 is a global standard for financial information exchange that provides a common language for financial institutions to use when exchanging information. The banks like ISO 20022 because it provides much better data, which makes software automation work much better and cuts down on manual processing.

Better data also helps banks keep track of information they need for regulatory reporting, and, for example, checking for money laundering and detecting and preventing fraud.

The original plan for ISO 20022 was that it was going to be rolled out, all over the world, by 2023. This was an ambitious timeline, and – not surprisingly – there have been some delays. Still, banks around the world are moving aggressively. In March of 2023, we begin the “coexistence period,” where the prior system will exist alongside ISO 20022. By 2025, all banks that want to participate in the international system must migrate fully to ISO 20022.

Blockchain is Crucial to the Adoption of ISO 20022.

SWIFT, the messaging system used by banks throughout the world, has been working hard to make sure that we don't live in a world of "digital islands" but that all of our systems, new and old, can work with each other.

According to SWIFT's Chief Innovation Officer:

Digital currencies and tokens have huge potential to shape the way we will all pay and invest in the future, but that potential can only be realized if the different approaches that are being explored have the 𝙖𝙗𝙞𝙡𝙞𝙩𝙮 𝙩𝙤 𝙘𝙤𝙣𝙣𝙚𝙘𝙩 𝙖𝙣𝙙 𝙬𝙤𝙧𝙠 𝙩𝙤𝙜𝙚𝙩𝙝𝙚𝙧.

SWIFT has been hard at work running pilot projects and expanding its system to ensure that it can "join up multiple distributed ledger technology platforms with each other, as well as with existing payment systems." They have recently released two reports

Connecting digital islands: CBDCs, Results of Swift experiments interlinking CBDC networks and existing payments systems to achieve global interoperability

Connecting digital islands: Tokenised assets, Results of Swift’s collaborative experiments interlinking multiple tokenization platforms to achieve global interoperability

Up to now, connecting two systems, i.e., the payment systems of two different countries, has required a complicated network of intermediaries. Every party has to verify and reconcile its accounts against every other party. This introduces delays, extra costs, and the potential for mistakes -- as anyone who routinely handles cross-border payments can attest.

A blockchain, or distributed ledger, eliminates the need for all the reconciliation and monitoring, and cross-monitoring. The shared ledger is the shared, definitive source of truth.

For more details on the great work SWIFT is doing to make all our systems interoperable, see their announcement "Connecting digital islands: Paving the way for global use of CBDCs and tokenised assets."

Meanwhile, watch this space.